ARGAN SA ($ARG.PA) is a French REIT that provides a 5.5% dividend yield right now, but additionally presents a possibility to continue to grow revenues sooner or later. The primary prospects of the corporate consist on nice well-known corporations like Carrefour, L’Oreal, DHL, Aldi, Decathlon, Amazon, or BMW.

Key Highlights:

ARGAN combines a excessive dividend yield with long-term income progress

Pores and skin within the sport: the administration owns over 37% of the enterprise

Making use of a good valuation strategy, ARGAN trades at a reduction

The enterprise mannequin:

ARGAN’s enterprise consists on renting premium logistics services. They will construct, develop or purchase warehouses, after which lease it, caring for the property administration throughout the entire lease. The corporate was created in 2000 by Jean-Claude LE LAN, who remains to be the Chairman of the corporate. Listed in 2007, proper earlier than the Nice Monetary Disaster, the corporate has returned over 321% plus dividends.

Pores and skin within the sport:

ARGAN is an organization with a market capitalization of 1.6 billion Euros. As we’ve stated earlier than, the founder remains to be within the firm, however not simply as an worker; his household nonetheless owns 37% of the shares excellent. This offers him and his household a long-term imaginative and prescient, since their wealth is tied to the efficiency of the enterprise. Predica, a subsidiary of Crédit Agricole Assurances, has owned 15% of the corporate for a very long time, serving as a superb counterweight for the household’s affect throughout the enterprise.

The present valuation:

ARGAN has generated 137 million Euros in Recurring Internet Revenue in 2024, up 9% from the earlier 12 months. Because of this the corporate is presently buying and selling at 11.6 occasions recurring earnings. For comparability, the present earnings ratio of the SP500 is 28 occasions.

The EPRA NAV NTA of the corporate, which is the Internet Tangible Worth of the belongings, stays at 85.5 Euros per share. With a present worth per share of 63.30 Euros, we’re buying the corporate’s belongings at a 35% low cost to honest worth. This worth has grown by 8% in 2024, and is anticipated to continue to grow in 2025.

For 2025, the corporate expects to extend its income by 6%, given new tasks and the listed will increase in worth of the present tenants; and its web recurring earnings by 11%, to 151 million Euros.

However is that this low-cost?

A good valuation:

ARGAN has a skillful administration that has overcome tough occasions just like the Nice Monetary Disaster whereas delivering distinctive returns to shareholders. Additionally, their wealth is tied to the enterprise, so they’re incentivized to make ARGAN a profitable enterprise.

I contemplate two methods to soundly strategy the valuation of ARGAN.

First, a a number of on the web recurring income. However there’s a trick right here. In 2021, the corporate managed to safe 500 million euros via a bond with a 1% rate of interest, which is due in November 2026. That is mainly free cash that the corporate is and has been utilizing. Nevertheless, as soon as the due date arrives, they’ll must refinance this cash. Most likely not the complete quantity, but when they did, refinancing at a 3.5% rate of interest would cut back web earnings by about 12.5 million euros.

Thus, I contemplate that the corporate’s earnings energy stays at 140 million Euros in 2025, being very conservative, which at a a number of of 15 occasions (in keeping with worldwide friends), offers us a margin of security of over 30%.

Second, it’s additionally honest to worth the corporate at e book worth. It will most likely be smart to use a premium to it, given the higher than the common high quality of the corporate’s belongings. However being conservative, and pondering of e book worth as a superb valuation methodology, the corporate additionally trades at a 30% low cost right now.

If the corporate traded at a premium, which I believe is probably going, the low cost might go as much as 57% utilizing a multiplier of earnings of 18 occasions, or to 48% if we utilized a ten% premium on the e book worth of the corporate.

Not every little thing is ideal:

Alternatives exist for a purpose within the inventory market. And I discover 4 causes for ARGAN to be low-cost:

1. Debt

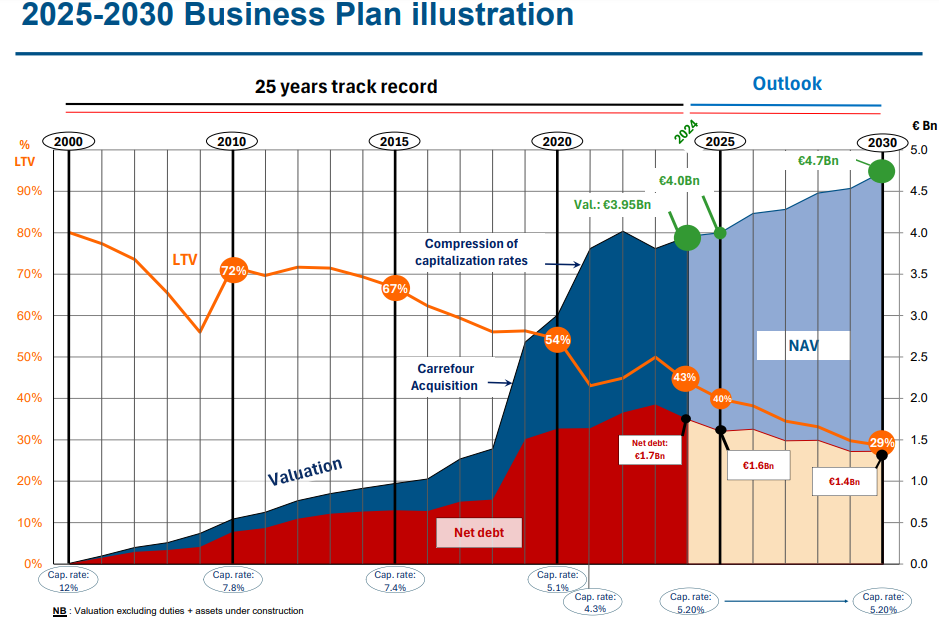

Though the corporate has been deleveraging its steadiness sheet recently, the debt to belongings ratio is comparatively excessive. The present Mortgage to Worth ratio of the corporate is 43.1%, which implies that debt funds 43% of the belongings; and the Debt to EBITDA ratio stays at 9.2 occasions. In 2023, these ratios have been 49.7% and 11 occasions, respectively, which exhibits the trouble of the corporate to deleverage the steadiness sheet whereas nonetheless paying over 3 euros per share in dividends.

The present price of debt is 2.25%, in contrast with 2.30% in 2023, and is anticipated to go all the way down to 2.10% in 2025. 22.13% of the rental earnings is destined to curiosity on loans, whereas 22.54% was destined in 2023.

Sooner or later, the plan of the corporate is to maintain decreasing the debt whereas investing to develop extra. They plan to finance new investments promoting their current belongings. The factors they’ll observe is: seniority (older services will probably be offered, ideally); profitability (services with decrease profitability will probably be offered, ideally); and ESG causes (services with greater CO2 emissions, that are sometimes older, will ideally be offered first).

2. Capital enhance

To battle the excessive affect of debt on the corporate, coupled with the upper rates of interest situation that we’ve lived through the previous two years, the administration determined to extend the capital in 2024. With a worth of 74 euros per share, the corporate created 2 million new shares, valuing the corporate at 1.7 billion euros.

Though the corporate disclosed that this capital enhance was focusing on new investments, it’s also a measure to adjust to their debt covenants and to take care of their BBB- score by S&P. Capital will increase are not often favored by traders, because it typically alerts overleverage and a possible mismanagement.

3. Writedowns

The French REIT trade has been impacted through the previous years of large writedowns. REITS are required to worth their belongings at honest worth, and in 2022 and 2023 ARGAN needed to writedown its belongings, decreasing its e book worth. In 2024 this pattern has reverted, though some opponents are nonetheless going via it.

The overvaluation of the e book worth is all the time a danger relating to REITs, and the latest writedowns have scared traders. Nevertheless, ARGAN isn’t too affected by this, because the services they personal are comparatively new (11.6 years as a median), and warehouses are much less affected by overvaluations than housing.

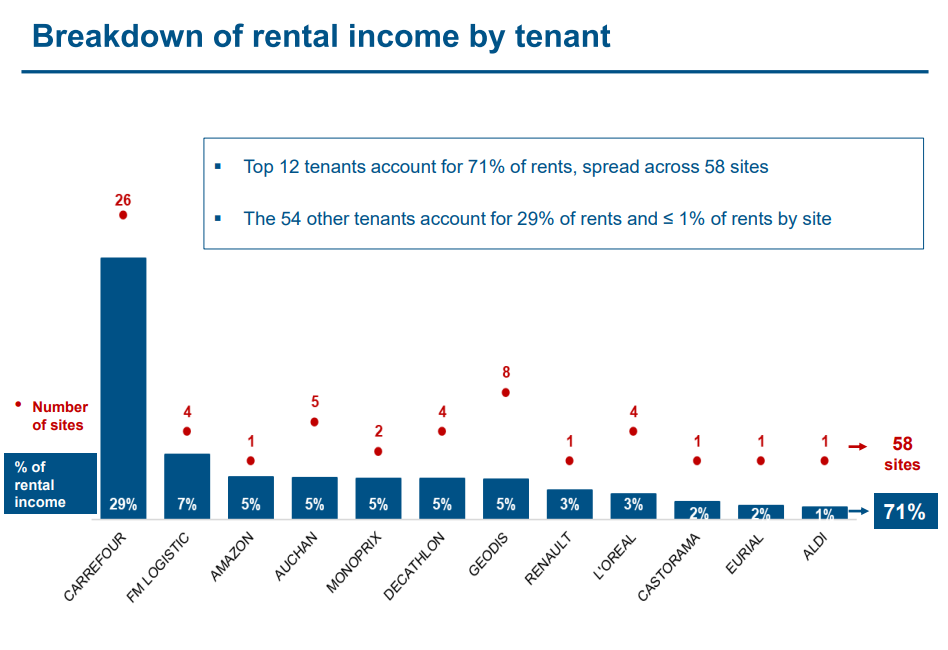

4. Focus of purchasers

Carrefour, ARGAN’s important tenant, accounts for 29% of the rental earnings of the corporate. This may occasionally pose a danger to the corporate in the long run. Nevertheless, the common fastened size of the leases is over 5 years, with 43% of the leases with a time period of over 6 years from 2024. Apart from, the corporate has been managing completely the occupancy ratio, which has been 100% previously two years, and hasn’t been decrease than 99% since 2016.

Conclusion:

ARGAN is a enterprise that’s buying and selling under its honest worth. With a reduction ranging between 30% to 50%, I believe that dangers are being overweighted by the market. The corporate has a stable historical past of income and dividend progress, even via tough occasions (Nice Monetary Disaster, pandemic). Moreover, the administration has pores and skin within the sport and a confirmed trajectory of being too conservative when releasing estimates. Though the primary focus right now is decreasing debt, I don’t discard (nor do they, based on their newest earnings name) that they change into extra aggressive with leverage and progress if a superb alternative comes.

Catalysts:

Decrease rates of interest

Enchancment of European financial views

Enchancment of S&P score (2026)

Time

If no catalysts happen, I’m nonetheless comfortable to be ready for the market to acknowledge the worth of an organization whereas receiving a 5.5% dividend yield and a web recurring earnings progress of excessive single digit.

Dangers:

Portfolio focus: Carrefour is an enormous a part of the income.

Debt: Though the corporate has traditionally had an occupancy charge near 100%, decreasing it to market requirements (about 95%, though it relies upon extensively on the regio) might imply difficulties in paying down the debt.

Problem discovering new developments.

How do you see ARGAN? Do you discover the dividend and the potential progress compelling?

I personal a place in ARGAN on the time of writing.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out considering any explicit recipient’s funding targets or monetary state of affairs, and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Price Prediction 2025 2026 2027")

Price Prediction 2025 2026 2027")

Price Prediction 2025 2026 2027")

{kind=link}