Amid a flood of headlines from the brand new US administration, buyers are sifting by means of key coverage strikes to know what is going to really affect markets. So, what have we discovered to date? Beneath, we spotlight the latest vital developments that we predict will have an effect on markets going ahead.

Tariffs: The US’s tariff strategy to China vs different nations is diverging, to date. Trump imposed a 25% tariff on Mexico and Canada to realize concessions however delayed implementation as soon as they complied. In distinction, a ten% tariff on China was enforced with out concessions. Most just lately, Trump mentioned a 25% tariff on all metal and aluminum imports could be introduced. Current worth motion and volatility means that the fairness market anticipates extended tariff retaliations. The tariffs may have vital impacts on US vitality companies, metal and aluminum consumers and sellers, and the general financial system. Shares within the automotive, know-how, shopper items, industrial, and luxurious sectors could stay beneath stress as a consequence of ongoing uncertainty. Firms like Ford, GM, Stellantis, Volkswagen, Apple, Walmart, Caterpillar, LVMH specifically, face provide chain disruptions, margin pressures, and general commerce uncertainty pausing capex intentions. Lastly, there’s a rising sense that Trump could transfer towards a common tariff on all imports later this 12 months which weighs on investor sentiment. We stay cautious as commerce tensions will proceed to affect company earnings and market sentiment.

Sovereign Wealth Fund: Most sovereign wealth funds (SWFs) are designed from present account surpluses, however the US lacks one. As an alternative, Treasury Secretary Bessent plans to monetize US steadiness sheet property to fund the SWF (pending Congressional approval). This might be a serious capital market occasion, enabling the US to purchase commodities, broaden globally, and probably put money into firms.

Financial Coverage: The resilient US labour market helps the Fed’s determination to carry charges regular, whereas the ECB and BoE proceed reducing key charges. This coverage divergence is predicted to drive markets by means of H1 2025. All central banks, nonetheless, stay data-dependent and centered on monitoring commerce coverage uncertainties for decision.

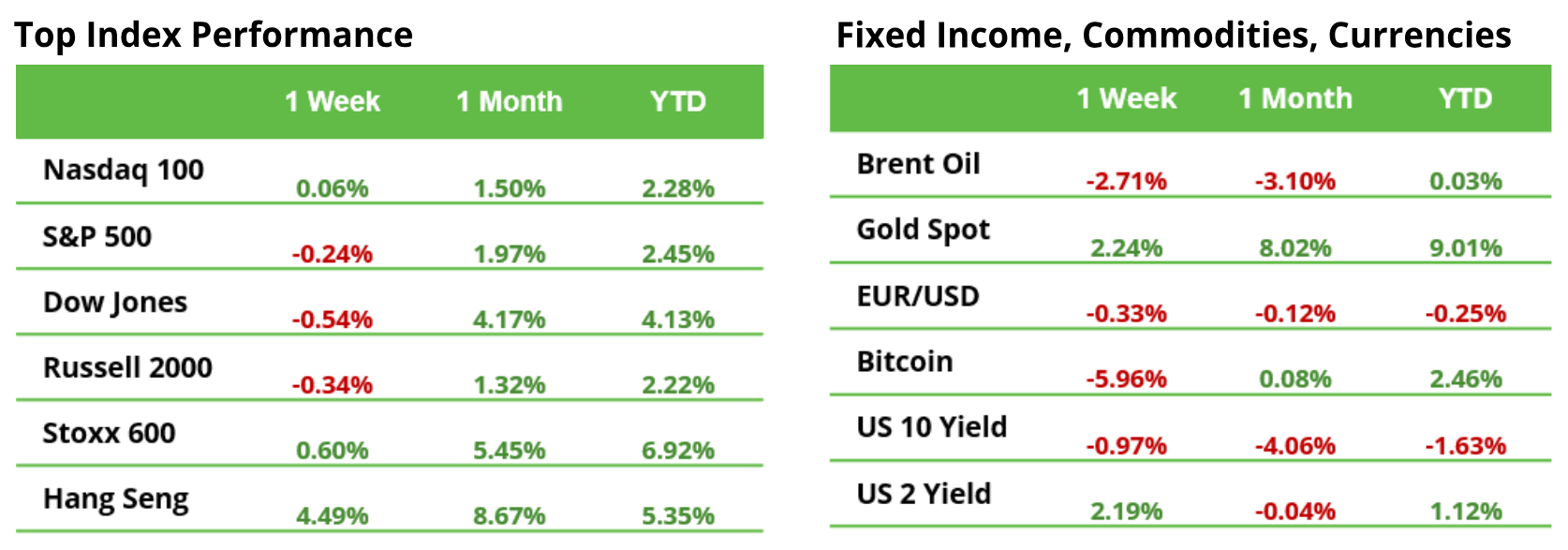

Earnings Season: After reporting final week, S&P 500 earnings development for the fourth quarter is predicted to be 12.3% with Communications and Financials the 2 strongest sectors. Income development can also be higher than initially anticipated, at 5.1%. Know-how is the chief from a gross sales perspective, however Well being Care is lastly displaying some indicators of life with revenues anticipated to be up 8.6%. This may be a welcome change for the index general.

Trump, commerce conflict and markets: a calculated threat with unsure dynamics

The U.S. commerce deficit has widened considerably in latest months, reaching a staggering $98.4 billion in December 2024. A pink flag for Donald Trump, who sees it as proof of the unfair therapy of the U.S. in world commerce. On the similar time, it highlights the immense significance of the U.S. as a key marketplace for different nations.

This improvement is prone to additional strengthen Trump’s stance. His purpose: harder measures to implement what he considers “truthful” situations. Though he has ignited the commerce conflict, he has not but escalated it. Tariffs in opposition to China are in place—however at a reasonable 10%. Deliberate 25% tariffs on imports from Canada and Mexico have been postponed on the final minute by one month. Whether or not they’ll truly be carried out or if Trump will improve the stress even additional stays unsure.

Nevertheless, greater tariffs usually are not the reply to his “America First” coverage—the financial state of affairs is much too complicated for that. Trump makes use of tariff threats as a tactical bargaining device to push by means of his pursuits. The markets appear to acknowledge this. After preliminary nervousness, the state of affairs has calmed down. The scary escalation has not occurred, and the “buy-the-dip” mentality, acquainted from the previous two years, stays intact.

Nonetheless, this gives a glimpse of what buyers can count on within the coming weeks—and presumably within the subsequent 4 years. Markets will proceed to be pushed by headlines, and uncertainty will stay a relentless issue. Whereas tensions have elevated, panic has not but set in. The S&P 500 closed final week lower than 1% beneath its file excessive.

Traders are torn. Nobody desires to tackle vital threat, however on the similar time, nobody desires to promote shares and miss the subsequent breakout to the upside. The sentiment? A cautious “wait and see.”

Earnings and occasions

Macro

12 Feb. US CPI; Fed Chair Powell testimony to Congress

13 Feb. UK GDP; Eurozone Industrial Manufacturing

14 Feb. Eurozone GDP; US Retail Gross sales

Earnings

10 Feb. McDonald’s

11 Feb. CocaCola, Shopify

13 Feb. Utilized Supplies, Siemens, Relx

This communication is for info and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any explicit recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Price Prediction 2025 2026 2027")

{kind=link}