Meet the “toll sales space” of digital transactions: Visa. The Each day Breakdown dives into this firm’s enterprise to see what’s happening below the hood.

Earlier than we dive in, let’s ensure you’re set to obtain The Each day Breakdown every morning. To maintain getting our each day insights, all it’s good to do is log in to your eToro account.

Deep Dive

Yesterday we regarded on the charts for Visa and at the moment we’re taking a deeper dive into the basics. Visa shares have struggled because the inventory hit a file excessive in June, down about 7.5%. Regardless of that, Visa is up about 26% over the previous yr and sports activities a powerful long-term observe file, up 368% during the last decade. For context, the S&P 500 is up “simply” 233% in that span.

The Enterprise

Traders know Visa as a credit score and debit card firm — that a lot is apparent. However it’s sometimes called the “toll sales space” of digital transactions. MasterCard enjoys an identical distinction. And whereas there are different bank card corporations — like American Categorical, Capital One, and Synchrony Monetary — additionally they perform as banks. Whereas there are professionals and cons to every enterprise mannequin, Visa and MasterCard command a lot larger revenue margins with their enterprise.

Progress

Visa has grown its income and earnings at a compound annual development price (CAGR) of 11.1% and 15.7%, respectively. Trying ahead, analysts anticipate spectacular outcomes as nicely, together with:

Income development estimates*: 11.4% in 2025, 10.6% in 2026, and 10% in 2027.

Earnings development estimates*: 15.3% in 2025, 12.3% in 2026, and 12.7% in 2027.

*Estimates in keeping with Fiscal.ai

Need to obtain these insights straight to your inbox?

Join right here

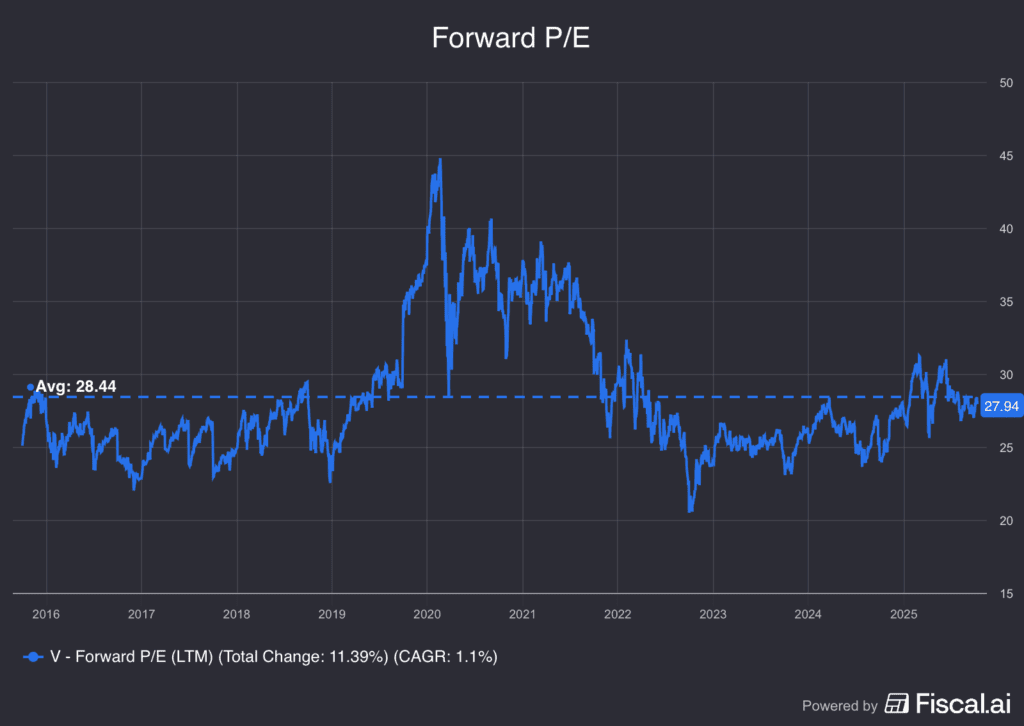

Diving Deeper: Valuation

Buying and selling at roughly 28x ahead earnings expectations, Visa inventory is about in-line with its long-term common. The inventory has been thought of comparatively low cost when shares commerce at about 23x to 24x ahead earnings and costly within the low- to mid-30x. Traditionally, many buyers have justified Visa’s premium valuation because of its elevated development charges and excessive margins.

Dangers & Backside Line

The principle dangers to Visa are fairly apparent: Market volatility and financial exercise.

If market volatility picks up, Visa isn’t immune. As an illustration, the inventory suffered a peak-to-trough decline of ~18.5% earlier this yr amid the tariff tantrum. Whereas this was truly higher than the S&P 500’s swing of 21.3%, it’s nonetheless an enormous swing.

The opposite danger could be an financial slowdown or a recession. As a result of Visa is a worldwide firm, a worldwide or US slowdown could be a destructive for a lot of companies — bank card corporations included — particularly in terms of consumption.

The Backside Line: Traders who consider Visa will proceed to generate robust top- and bottom-line development might justify the inventory’s valuation, which is at a slight premium to the S&P 500 however roughly in-line with its long-term common. Those that view the inventory as unattractive at present ranges might await Visa’s valuation to probably dip to a extra enticing stage or they could not like Visa’s enterprise and resolve to ignore it altogether.

Disclaimer:

Please observe that because of market volatility, a few of the costs might have already been reached and eventualities performed out.

Price Prediction 2025 2026 2027")

{kind=link}