Hey Everybody!

There’s been a whole lot of noise recently round Google ($GOOGL). Between lawsuits, AI battles, and aggressive headlines, it’s simple to surprise: Has Google misplaced its moat? For a lot of, the story has shifted from “invincible tech large” to “dinosaur underneath siege”, with some headlines evaluating it to Yahoo within the 2000s.

I get the issues… Epic Video games trials, DOJ respiration down their neck, regulators in Europe getting extra aggressive, and Microsoft ($MSFT) with OpenAI — it’s sufficient to make anybody hesitate. Even YouTube is underneath strain, combating for consideration in opposition to TikTok.

However right here’s the factor — when everybody’s wanting on the headlines, getting brainwashed by the noise… I prefer to look underneath the hood of the automobile, identical as I do after I hear some bizarre noise in my previous Toyota Prado 2006. So let’s have an in-depth look:

The Noise: AI Wars, Lawsuits & Dangers

U.S. Division of Justice (DOJ) antitrust case

E.U. investigations, lawsuits and costs

Intense AI competitors from powerhouses like OpenAI, Microsoft, and Meta

Rising competitors in Search from AI-driven options (Chat GPT)

YouTube’s battle with TikTok for consumer consideration

Aggressive cost-cutting and layoffs in non-core “moonshot” tasks

In 2022 and early 2023, ($GOOGL) underperformed as rates of interest rose and margins compressed. Wall Avenue doubted its means to adapt. Nonetheless, we see one thing completely different: a fortress enterprise presently at a uncommon valuation disconnect.

Key Highlights: Why Google Stays a Powerhouse

Regardless of the noise, Alphabet (guardian firm of Google ($GOOGL)) continues to dominate in essential areas:

Dominates 90%+ of world search through Google.

Owns market-leading platforms: YouTube, Android, Google Cloud, Gmail….

Compelling valuation: lower than 20x earnings with an enormous internet money place.

Gemini AI is deeply built-in throughout Workspace, Cloud, and Adverts.

Nonetheless rising income at double digits – even at a colossal $300B+ scale.

Value self-discipline: over $7B in annualized financial savings from layoffs and efficiencies.

Sturdy capital returns: $70B+ in share buybacks as margins get better.

Possesses one of many strongest stability sheets globally.

Enterprise Mannequin Overview: Unpacking Google’s Moats & Competitors

🔒 Google’s Enduring Moats

Search Monopoly: As talked about above.

Information Benefit / Community: Billions of customers and information throughout platforms.

Scale: Google has an enormous scale and money to compete and outrun others.

Excessive Switching Prices: Google companies are deeply embedded in consumer workflows.

Supply: Rand Fishkin @randderuiter on X

⚔️ Key Opponents

Whereas fierce, Google ($GOOGL) maintains dominance because of unmatched scale and distribution.

Search: Microsoft ($MSFT) (Bing + OpenAI integration)

Video: TikTok, Netflix ($NFLX), Instagram ($META)

Cloud: AWS ($AMZN), Azure (Microsoft)

AI Basis: OpenAI, Anthropic, Meta

Autonomy (Waymo): Tesla FSD ($TSLA)

🧱 Key Strengths

Alphabet’s ($GOOGL) energy isn’t simply in its model — it’s within the structure of the web. Google Search, Maps, Android, Chrome, YouTube — these aren’t simply companies. They’re habits. They’re defaults. The form of instruments individuals don’t simply use — they rely on. That dependency is highly effective. It’s why regardless of all of the competitors Alphabet retains rising.

Alphabet’s energy can be in scale and adaptableness. Google is investing closely in Propietary TPUs for AI compute, Information Facilities, AI throughout Search, Workspace and Adverts. Google tradition of adjusting and shaping requirements will guarantee they constantly attempt to invent.

Fundamentals & Technicals Guidelines: A Deeper Dive

Earlier than I put money into any firm, I’m going via a full guidelines — not simply to see if the numbers look good, however to actually perceive how the enterprise works and why/the way it would possibly develop over time.

I don’t depend on hype, headlines, or AI-generated content material. I prefer to depend on key information, traits, and monetary well being. This guidelines I constructed primarily based on guidelines helps me break issues down throughout fundamentals, valuation, profitability, administration, and even technical indicators. I give every line merchandise a rating, to not be overly scientific — however to remain constant, take away emotion, and make higher selections over the long run.

If an organization doesn’t meet my requirements, it doesn’t make it into my portfolio. It’s that straightforward.

🧰 Monetary Power: Google ($GOOGL) A True Fortress Constructed to Final

Investor Confidence: Huge funds like Ackman, Klarman, Griffin, Loeb are invested.✅

Earnings & Valuation:

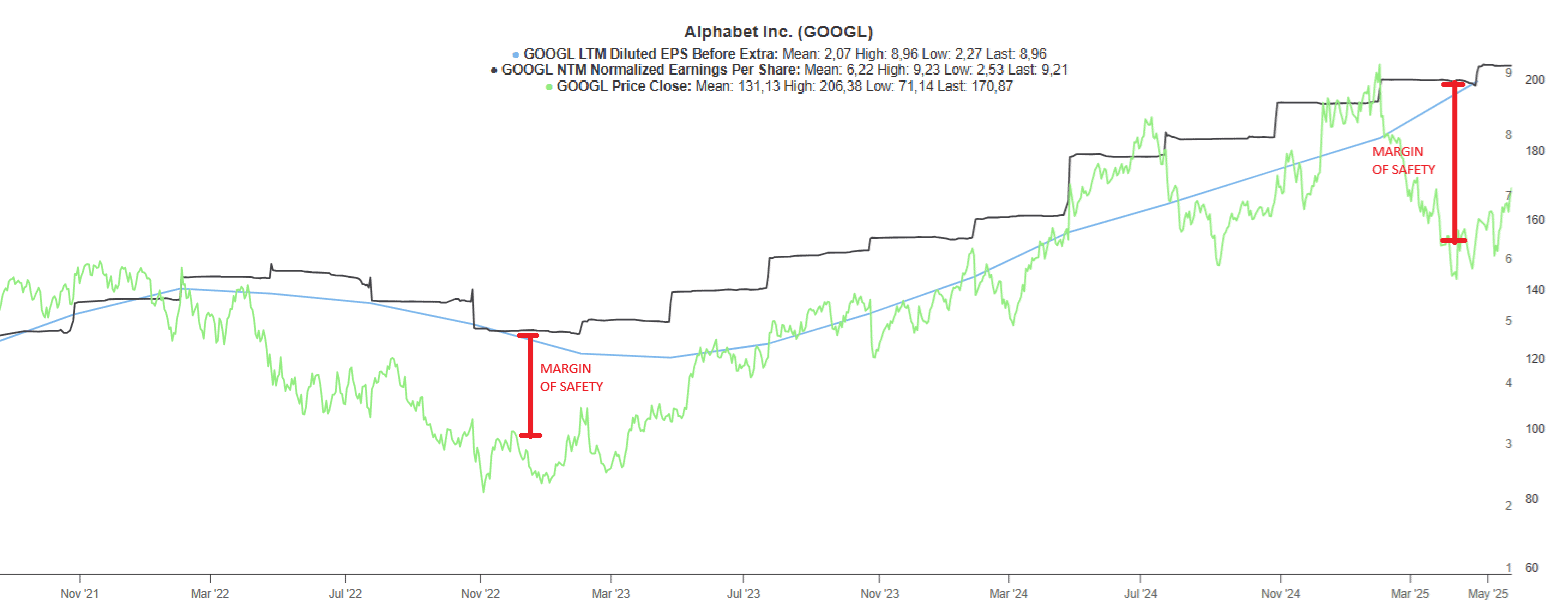

EPS (TTM) is $8.96 // P/E round 17x. ✅

Projected development of 15% CAGR suggests a good P/E as much as 28x, providing a major margin of security. ✅

Earnings are steady and rising, from $5.80 in 2023 to ~$8.96 in 2025. ✅

Supply: TIKR Terminal. Graph reveals the deviation in valuation and the margin of security.

Profitability & Margins:

Working Margins are 32.7%, up from 25% in 2015, constant development. ✅

Whereas aggressive, Meta and Microsoft margins are increased. 🟨

Return on Fairness (ROE) is 34.6%. ✅

Debt: With a low Debt-to-Fairness ratio of 0.07x and $74.9 billion in free money movement (TTM), Google has immense monetary flexibility. ✅

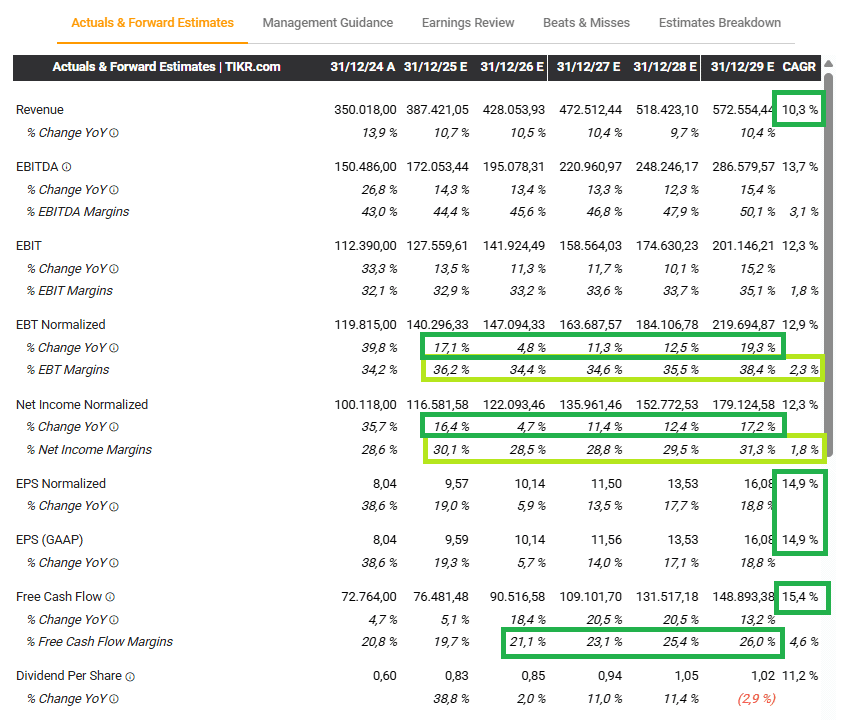

Supply: TIKR Terminal. Analysts anticipate subsequent 5 years of double digits development and margin enlargement

Enterprise Mannequin & Moats: Their sturdy financial moat comes from model, information, scale, and consumer switching prices. As per my guidelines a (4/5 rating) ✅

Resilience & Administration: Google ($GOOGL) rapidly recovered from previous crises, demonstrating sturdy resilience. Administration is very aligned with shareholders, with founders retaining vital voting energy and CEO closely tied to inventory. ✅

Shares buy-backs: Purchased again $15 billion in regular shared final quarter. ✅

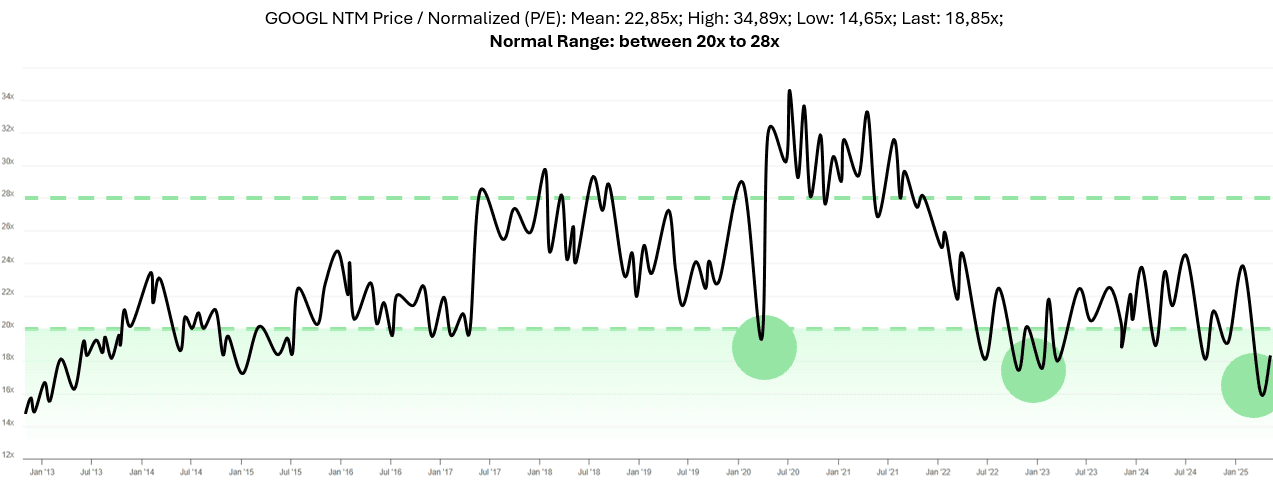

Engaging Valuation: A P/E of 18x and EV/EBITDA of 12.5x are under the thresholds for this development, suggesting good worth and margin of security ✅

📉 Technical Evaluation: The Worth Tells a Story

The inventory’s value motion reinforces confidence in its trajectory.

Constant Development: Google ($GOOGL) has proven a constant uptrend over 10 years, with common annual development fee of ~18.6%, typically hitting All-Time Highs. ✅

Favorable Entry: The present value may doubtlessly be an excellent shopping for alternative at NTM Ahead P/E of 18x. ✅

Supply: AMWorld,utilizing datasets from TIKR

Diversification Notice: Whereas sturdy, Google’s tech focus means it may not diversify your portfolio a lot when you’re already tech-heavy. ❌

As a part of this rule-based guidelines Google ($GOOGL) scores excessive over the minimal 70% that I anticipate for any firm to have the ability to be part of the listing of “Worth Development Compunders” a the ultimate scores sits at:

Alphabet ($GOOGL): ✅ Closing Rating: 89/100 – EXCELLENT!

What concerning the Future?

Actual Dangers (And Why I’m Watching Intently)

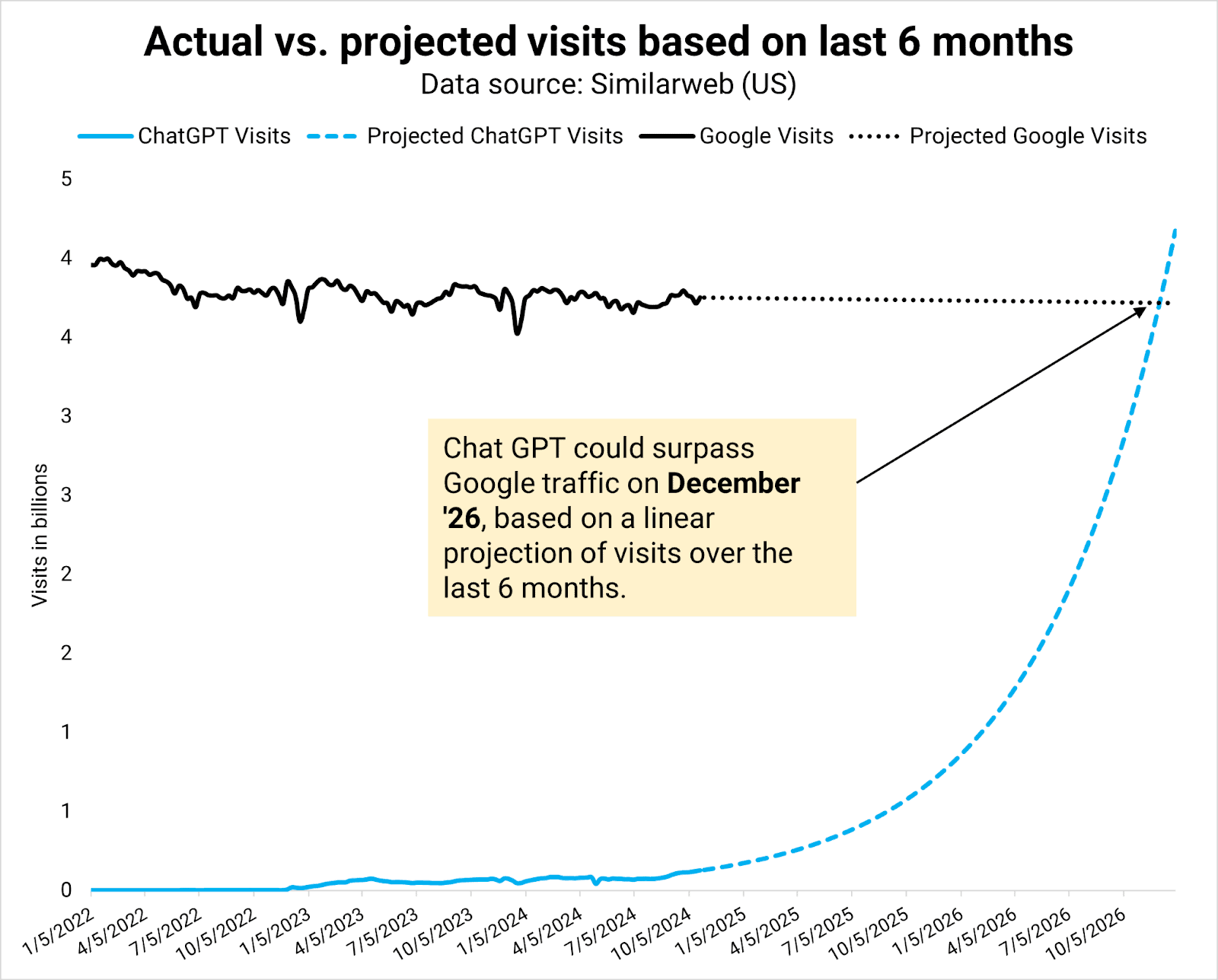

I’ll be trustworthy — if there’s one factor that retains me up at evening about Google ($GOOGL), it’s the shift in how we seek for data. For the primary time in a long time, Google Search feels weak. Instruments like ChatGPT and different generative AI fashions have utterly modified the best way individuals work together with the web. As a substitute of scrolling via ten blue hyperlinks, you ask a query — and the reply simply seems. It’s quick, pure, and in lots of circumstances, extra useful than a standard search end result. If this shift continues, and extra individuals get used to AI-first search experiences, Google ($GOOGL) may face actual disruption to its core enterprise — the one that also brings in most of its income.

Supply: growth-memo.com / gpt-search. ChatGPT forecasted development

That’s not one thing I take frivolously, and it’s a danger I’m watching very carefully by understanding key metrics and KPI’s on AI and search utilization at each quarter. However when you assume twice historical past equally repeats, and comparable has occurred already with the video app Zoom $ZM, the result… $MSFT with it’s scale and community took them out of the race by together with Groups at no cost of their workspace package deal.

Outlook for the Future: A Generational Compounder?

With Google Search, YouTube, and Android, Alphabet controls the basic “pipes and platforms” of the web. This immense energy, mixed with its rising AI management and disciplined capital allocation, may rework it right into a generational compounder. as the entire main AI productiveness suite supplier: Gemini + Workspace + Cloud + Adverts. The last word free-AI full office.

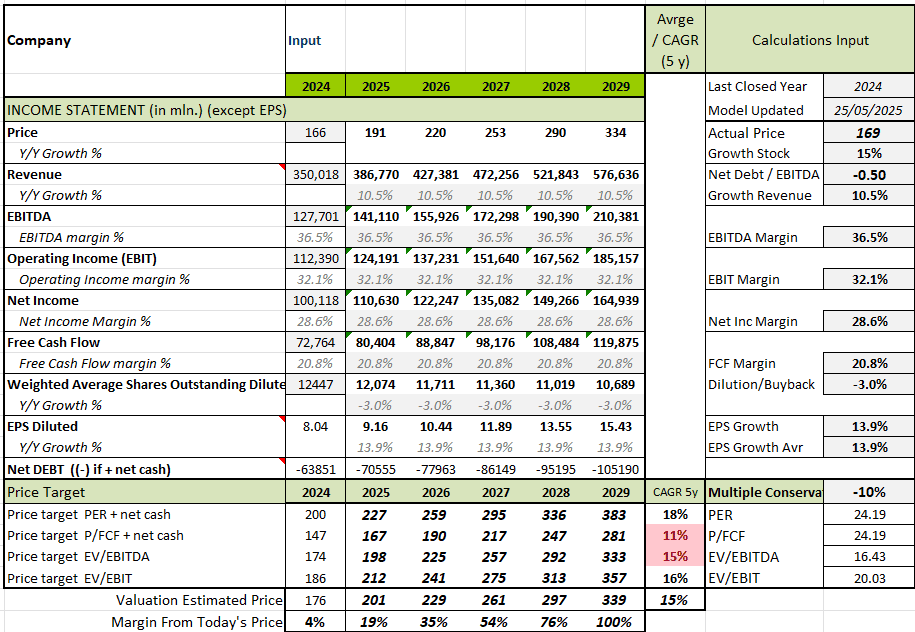

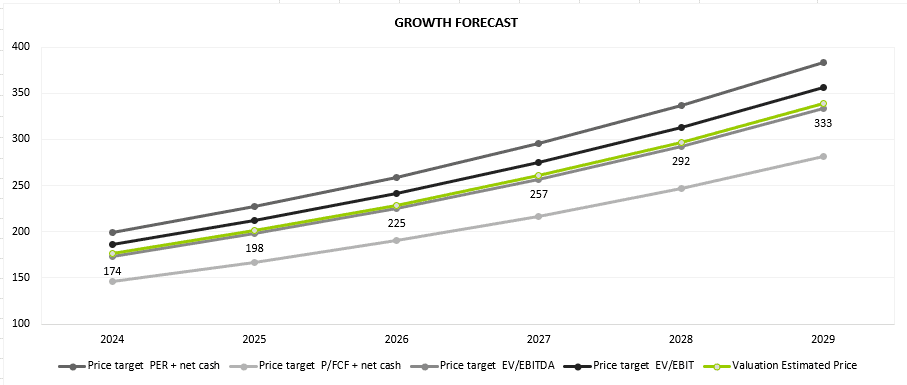

🎯 My Forecast Worth: A Conservative Estimate

After analysing an organization rating, I’m going then to analyse its intrinsic valuation and its forecast over the subsequent 5 years. On this case, for this evaluation I’ve not taken under consideration any margin enhance. That is my “Regular” situation primarily based, “Bear” and “Bull” circumstances are extremes I could share sooner or later.

Supply: AMWorld

($GOOGL) Forecasted 5-Yr CAGR > +15% ➔ Glorious long-term development potential!

✅ Conclusion: A Misunderstood Compounder

So after this evaluation, similarly as after I hear some noise in my 20 12 months previous Toyota Prado, I examine underneath the hood, and I realise after checking all the things with the mechanic, that these are regular noises of each day operations and {that a} Prado is a automobile constructed to final, identical as Google ($GOOGL). Each round 20 years previous, however nonetheless with a whole lot of potential. Each had been constructed to final.

In any case, after this humorous comparability of my previous automobile with Google ($GOOGL)…

I’ve seen this sample earlier than — with Netflix, Meta, and now Google. The market overreacts to vary. Most buyers get caught up within the noise: lawsuits, TikTok, the AI arms race. We select to concentrate on the sturdy fundamentals. Alphabet ($GOOGL) is undeniably a top-tier enterprise presently buying and selling at what we think about mid-tier valuations. And that’s the place long-term buyers discover their edge.

Google with its scale, adaptability and MOATs will nonetheless be one of the vital essential corporations within the digital world in 2, 5 and 10 years.

🟢 My Verdict: A Excessive-High quality Compounder. Alphabet – Google ($GOOGL) stays a core place in our portfolio.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out taking into consideration any explicit recipient’s funding aims or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Price Prediction 2025 2026 2027")

{kind=link}